Solving the investor’s dilemma – managing volatility in equities (Part 1)

Dan Bosscher, Portfolio Manager at Perennial Value Management discusses risk management in client portfolios and how embedding risk within an equity portfolio can help reduce the impact of market drawdowns. (Read part 2 here).

Equity investors face a constant dilemma: how can I achieve the long term returns that equities can provide, without the capital loss that accompanies market downturns? This question has become particularly pertinent following the GFC and its dramatic impact on share markets. The Australian equity market lost 50% of its value between the peak in November 2007 and March 2009 when the market bottomed.

While most investors appreciate the impact of the loss of capital, they tend to overlook the secondary impact; they now earn future returns on a reduced amount of capital. Over time this can have a significant impact on investment outcomes.

Risk management in client investment portfolios has traditionally been an asset allocation decision. Indeed, for an overall “balanced” portfolio asset allocation may work to an extent, cushioning portfolio volatility through diversification. But why wouldn’t you seek to manage volatility within an equity portfolio?

Most long only managers are employed to generate ‘alpha’ above an equities benchmark. ‘Beta’, the risk arising from exposure to general market movements, is someone else’s concern (typically the asset allocator putting together the investor’s portfolio). Why then was the average investor unhappy when their equity fund halved in value in 2008? After all, their manager had a mandate to be at least 90% invested in equities, regardless of how bearish they may have been. The simple answer is that conventional equity products do not meet all investors’ expectations during such difficult times.

Numerous studies have shown that the pain of losing money is greater than the joy of making it. But emotions aside, the loss of capital is a serious matter. In our view ‘risk’ is the probability of losing money, not just volatility. It took almost six years for the market to return to its November 2007 high on an accumulation basis. If you had invested at the pre-crisis peak, this equates to a 100% return – a return that only gets you back to where you started.

This dilemma is most important for those investors approaching retirement. For these investors the possibility of loss can pose a more significant problem. The issues arise where the pattern of equity market returns is such that large negative returns occur early in the drawdown phase causing investors to eat into their capital such that they do not get the full benefit when markets inevitably rebound. This is known as ‘sequencing risk’. Given that we are in retirement for longer, we need to make sure that when we do retire our asset base is as healthy as it can possibly be. What that means is that as we approach retirement age we need to be even more mindful of losing capital. Hence, while risk management is always important, it is even more important in the pre-retirement phase and in the early years of retirement.

One common solution proposed to reduce the impact of negative market movements in the retirement phase is to adjust the asset allocation mix by decreasing the allocation to growth assets and increasing the allocation to defensive assets. But will a portfolio skewed towards fixed interest assets be able to deliver the growth required to sustain a long and comfortable retirement? Does trying to solve the issue of sequencing risk in this manner just open up a new risk – longevity risk? That is, the risk that you will outlive your nest egg. With life expectancies growing and the cost of living rising, more than ever our retirement nest egg needs to be maximised, both at the start of retirement and throughout the drawdown phase. Therefore reducing exposure to growth assets may not be the solution.

Alternatively, some investors believe that timing is the solution to protecting their capital in market downturns. “I will just pull my money out of shares and put it into cash, then put it back into shares when the market turns”, right? Wrong. Perfect timing is impossible to achieve without the benefit of hindsight.

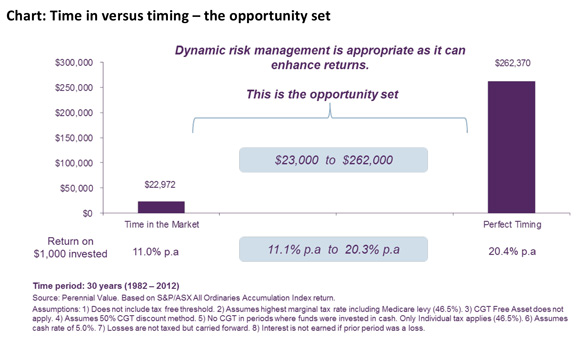

The chart below shows the impact that timing can have on returns. Consider $1,000 invested in the Australian share market over 30 years (left hand bar). By staying invested over the whole 30 years the investment would have grown to be worth almost $23,000 (after tax at the highest marginal rate) or an 11.0% p.a. return. At the other extreme (right hand bar), consider a situation where with perfect hindsight, moving in and out of the market at exactly the right time (which of course is all but impossible to do) would have produced more than $260,000 (equivalent to a 20.4% p.a. return); over 10 times the dollar amount achieved by just staying invested in the market over the 30 years. While perfect timing is unrealistic, it does illustrate that there is a significant opportunity to improve our long term returns if we as investors can better manage the risk of losing capital during periods of significant market downturn. The key is to try and stay invested, but find alternative ways to reduce your effective exposure when needed in a market downturn.

In the example below, the opportunity set that arises by better managing the capital risk of your portfolio lies between $23,000 and $262,000. It is within this opportunity set that we believe dynamic protection can help enhance returns.

An important point here is that timing affects your market participation, and you need to maintain good market participation in order to maximise future returns. But attempting to time the market is very challenging. It is neither a rational or likely achievable strategy. Risk management can produce a better and smoother outcome for investors, in our view.

Managing the downside in equity portfolios can be the difference between staying in front, and falling behind, perhaps forever. We believe the best of both worlds is to have a risk management strategy that allows investors to benefit from the superior long term return of shares, while having a dynamic protection strategy in place to help reduce the impact of market drawdowns.

At Perennial Value, we believe risk should be managed both within equity funds as well as via asset allocation changes. In some cases, particularly for retirees, it makes sense to embed risk management in the form of simple insurance style instruments into the equity portfolio itself. The aim is to manage the risk of equity market downturns automatically, without the investor having to make a conscious decision to change asset allocations.

In part two of this article we will discuss the strategies utilised that make it possible to embed risk management within an equity portfolio and how this can provide investors with a degree of confidence to remain invested in equities, regardless of market volatility or their proximity to retirement.

————————